Market implied recession probabilities; Earnings season back in full swing with some heavyweights reporting; US, EU Equities down, Nasdaq retakes its leadership, Japan up on BOJ.

Major market events 23rd – 27th January 2023

Highlights for the week

Mon: Australia PMI. Canada New Housing Prices. ECB Lagarde speaks.

Tue: S&P PMIs US, Germany, EZ & UK. Germany 5-year & US 2-year auction.

Wed: Germany IFO, BOC rate decision. Australia / New Zealand CPI. US 5-year auction.

Thur: US GDP 4Q. Tokyo CPI, US 7-year auction.

Fri: US core PCE, Sweden unemployment.

To Watch: Earnings reports Q4 will gain center stage with some of the heavyweights reporting. Federal Reserve speakers will be in a blackout period ahead of the February meeting, but ECB has a few speakers including Madame Lagarde, and economic data will set the expectations around recession probability.

Market-implied Recession Probabilities.

Despite a volatile week, market-implied recession odds are much lower than a few months ago.

Source: JPMorgan

What it is probably worthwhile noting while reviewing market pricing across asset classes:

– Credit stands out as an expensive asset class, especially when compared to equities.

– Furthermore, QT is probably a bigger problem for credit rather than equities. Against this macro backdrop, I would expect credit to face greater headwinds than equities.

– What also stands out is the expansiveness of HY compared to High Grades. The 3Y rolling window z-score of the spread between BB and BBB in the US is reaching almost -1 sigma. Meaning that BBs are significantly expensive vs. BBBs on a historical basis.

– The only segment of US credit that is not trading well below long-term averages is CCCs. That’s the only credit segment that could provide a further impulse to credit indices. Other than that, the spread tightening feels pretty much done!

Earnings Calendar Highlights

After the vigorous start of the year, last week there was a pause in most equity markets. Yields started to climb once more, and equities are very sensitive to rates at the moment, so that created a headwind. The big decision of the BOJ to keep its ceiling at 50bp prompted a rise in Japanese stocks – which had the best returns for the week. Prompted by a bullish report from Netflix, US markets managed to end the week on a high note, with Nasdaq reclaiming its leadership and with the S&P 500 reconquering 50 and 200 DMA. The next week will lead us to the Federal Reserve meeting of Jan 31-Feb 1 and – while there are expectations for further moderation in rate hikes –

this will be a crucial milestone to determine the market’s direction going forward, at least in the short term. On a longer-term basis, we are dependent on data and it will be a particular focus to see if 1) there will be a recession and 2) by how much US corporate earnings estimates are going to be cut. We certainly live in very interesting times.

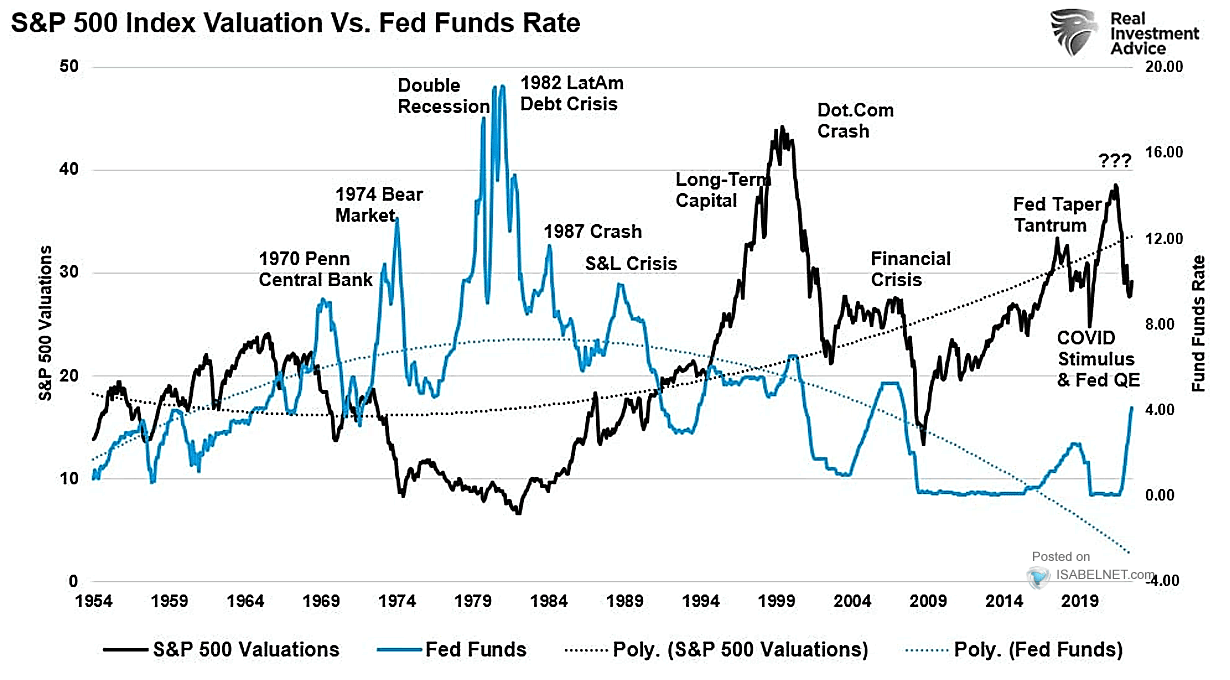

Source: Real Investment Advice

Back to the elephant in the room (the Fed). The chart above shows that increases in Fed Funds are particularly relevant when valuations are high. At the moment these are slightly below the 5-year and 10-year average, but the risk is they could rise meaningfully were the estimates to be cut significantly. This week saw the return of growth concerns, partly because of the mixed messages from China in terms of GDP growth and population growth. Furthermore, some of the major tech bellwethers (Google and Microsoft) announced significant cuts to their workforce during the week. As mentioned before, Netflix did manage to set the tone right by the end of the week. Will it last?

Source: Real Investment Advice

More on recession – 90% of the US yield curve is inverted, signaling an upcoming recession. Will we get one, or the economy will manage to perform a soft landing? Opinions differ on this point, with Goldman Sachs saying there is only a 35% chance we will have a recession, Bank of America (see below) forecasting a mild recession, and Morgan Stanley opting for a more severe recession with a significant cut to earnings. Looking at the current earnings report, it does not seem that things are going so badly even though 4Q22 is going to be the first quarter of negative growth since 3Q20. What strikes me is that very few companies have issued guidance for 1Q23 (and when they did it was mostly negative) which possibly means that we will have to learn how robust the economy really is as we go. Governor Powell’s opinion was that the economy was sufficiently strong to withstand some rate hikes – let’s hope he’s right!

Source: BofA Global Research

The forecast from BofA shows a contraction for three quarters, and one does wonder where inflation is going to be in that scenario and whether the Fed will eventually cut rates as the market is currently pricing in. The dip wouldn’t be disastrous as it was in 2008, but still would reduce earnings meaningfully and, in all likelihood, compress the multiple. Ironically this would happen just as the Fed reached the peak in Fed Funds in May. This would probably still leave 2023 with positive GDP growth, but earnings and the market won’t definitely like it.

Source: BofA Global Fund Manager Survey

I hope that’s not all doom and gloom ahead for us – we’ve had plenty of that last year! On a more positive note, it looks like recession fears have peaked, according to the Bank of America survey. The economy has been mostly resilient lately, and in fact, the current positive pace is forecasted to continue for at least a couple more quarters. The job market seems to be resilient even in the face of technology’s massive layoffs, which should sustain the economy with inflation hopefully moderating further.

Source: Carson Investment Research, FactSet

Another potential source of support could come from the government, as President Biden positions for potential re-election in 2024. Still, with the current split in power, as Republicans retook the House in the mid-term elections last year, it won’t be easy for the government to increase spending. This is a positive data point to consider anyway.

Source: Topdown Charts, Datastream

Source: ISABELNET.com

In terms of sentiment, the bears do have the upper hand at the moment, even in light of January’s positive start. Near term, I think the outlook depends on yields (as well as earnings), as lower yields do support the market. Last week we had one negative earnings report from Goldman Sachs and a positive one for Morgan Stanley – not enough to draw a stance on the whole sector, as the issues seem more relative to positioning and company-specific rather than market or sector-specific. Next week will be full of earnings reports and hopefully, we will be able to gauge precious insights about how the rest of the year will unfold.

Source: Carson Investment Research, Factset

The above chart seems to be eerily predictive of what could happen next week – a bad week because of subpar earnings and then the Fed comes to the rescue (!) by hiking the Fed Funds rate by 25bp? For sure it will be very important to watch closely the reports from technology, financials, and healthcare companies next week. I’m anyway certainly hoping this doesn’t spoil the party, as it would be very important for the markets to close January in the black.

Source: Compustat, Goldman Sachs Global Investment Research

It should come as no surprise that the ROE is falling – the decline has been consistent throughout the year. The decline has been more marked for the financials, while the rest of the market seems to hold up quite well. I would note that the absolute level is at an all-time peak, meaning that the companies managed to recover well after the financial crisis. The recent decision of tech bellwethers mentioned before to downsize in the face of very solid results may point to this too.

Source: FactSet, BofA US Equity & Quant Strategy

Margin expectations have been cut as consumers are feeling the pinch from higher rates and companies can no longer pass on all increased costs to the consumer. Still, as per the ROE above, I would note these are quite healthy especially considering they might come right before a possible recession. Hopefully, this moderation in forecasts will allow companies to meet easier comparisons.

Source: FactSet

The forward 12-month P/E ratio for the S&P 500 is 17.0x, down from 17.3x last week, which is below the 5-year average at 18.5x but above the 10-year average at 17.2x. Earnings seem to hover around the $ 230 mark lately, but it is clear that the next three weeks will bring meaningful revisions as 4Q22 unfolds. There we will probably understand how the economy is shaping up for 1Q23 and beyond.

For 4Q22 the forecasted EPS decline for the S&P500 on aggregate is -4.6% – revised downwards from -3.9% a week ago. If correct, it will mark the first time there has been a year-on-year decline since 3Q20, when such a decline was -5.7%. Despite the concern about a possible recession next year, analysts still forecast a positive growth in earnings for the overall market in CY 2023 of 4.2% year on year, again revised downwards from 4.6% last week.

Source: Factset

Very few sectors are holding up estimates relative to just 3 months ago. The only sector not to have its estimates cut further is Consumer Staples; all the others are facing cuts. Even with positive reports from most banks financials had their estimates for the year cut to 13%. Still, that’s the group with the second-highest growth forecasted for the year.

Source: Factset

The S&P 500 has its revenue growth estimates trimmed further to 2.9% from 3.2% one week ago. Financials are leading the pack in terms of revenue forecasts, and are the only sector to have a higher revenue forecast relative to the end of 2022, with Utilities being unchanged and all other sectors being down.

Source: Factset

Introducing EPS for 2023 and 2024, which surprisingly took a downward revision recently. The forecast for 2023 – which has held steady since mid-November when the first figures ($ 229) were published – has now been updated to $227.6; while 2024 has had a cut of the same measure from $ 254 to $ 251. I look with much interest at further revisions as the 4Q22 report season gets underway.

Source: Factset

This is the detail for 1Q23. While the market might be more concerned about rates and recession than is about earnings at this point, the latter’s deterioration is starting to get me worried. I will be looking at next week’s report with much interest.

The earnings season is now entering in full swing its 4Q22 reports. Highlights this week include Microsoft (Tuesday, After Close), Texas Instruments (Tuesday, After Close), Tesla (Wednesday, After Close), MasterCard (Thursday, Before Open), Intel (Thursday, After Close), Visa (Thursday, After Close), and American Express (Friday, Before Open).

Source: Earnings Whispers

Market Considerations

Source: BofA Global Fund Manager Survey

Indeed the market took a breather last week, but the bulls’ hopes managed to be intact by the S&P 500 retaking 50 and 200 DMA. Apart from the overwhelming macro considerations I am increasingly worried by the reduction in earnings forecasts, even though I note that the S&P 500’s P/E managed to decline slightly this week. The upcoming earnings can be a double-edged knife: on one side the economy has been strong, but fundamentals are beginning to deteriorate and layoffs abound. I would still stay on the sidelines next week, although I am aware I might well miss an opportunity if some of the key reports are going well. Will continue to watch closely the 10-Year yield after a meaningful climb last week. Continue to prefer US over Europe and Japan, even though the latter can get some respite from the BOJ’s decision to enforce its current ceiling for JGBs. To those who were invested since the beginning of the year, congratulations – I’d probably take some short-term profits here, looking to re-enter the market if there is a slide of 4-5% in the S&P 500. The very impressive rally in equities has somehow changed my previous preference for bonds, but I still think that long (US) bonds is probably the easier trade here with less volatility, while for those who can stomach higher volatility and a longer investment timeframe it might make sense to test waters in equities. Just to mention that it is way too early to call this the bottom in equities – we definitely need more confirmation on the outlook both from the macro and the micro perspective. For the less volatility prone of you, it may make sense to take all opportunities to lighten up in equities and reinvest in bonds at attractive (approx 3.5-4%) yields.

Happy trading and see you next week!

InflectionPoint

Disclaimer

All views expressed on this site are my own and do not represent the opinions of any entity with which I have been, am now, or will be affiliated. I assume no responsibility for any errors or omissions in the content of this site and there is no guarantee for completeness or accuracy. The content is food for thought and it is not meant to be a solicitation to trade or invest. Readers should perform their investment analysis and research and/or seek the advice of a licensed professional with direct knowledge of the reader’s specific risk profile characteristics

Leave a Reply