Stocks fall, rates fall, and bonds have a positive week; hawkish Fed means that the peak rate might reach 6%; NFP above consensus but unemployment rises. Watch out for CPI and PPI on Tuesday and Wednesday.

Major market events 13th March – 17th March 2022

Highlights for the week

Mon: IN CPI.

Tue: US CPI.

Wed: CN Industrial Production, UK Spring Budget, US Retail Sales, US PPI, NZ GDP.

Thur: US Jobless Claims, Philadelphia Fed Manufacturing Index, ECB Interest Rate Decision.

Fri: EU CPI, US Industrial Production, US Capacity Utilization.

Performance Review

Well, that was quite a bloodbath, particularly as the US is concerned. In the week where we got the scent that interest rates will be much higher for longer, and where NFP were once again ahead of consensus, rates did come back a little, but equities did come back a lot, with the S&P breaking the 100-day moving average once again. The week started with Governor Powell’s semi-annual testimony in which he set the scene for interest rates being raised at a higher level than it was previously thought in order to bend the labor market and tame inflation. After his testimony, the market repriced rates again, and Goldman Sachs added 25bps to their forecast to a peak of 5.5-5.75%, in line with what is currently priced by the market. Irrespective of whether the March hike will be by 25 or 50 bps, the Fed will open the door to a longer hiking cycle than previously thought, and Goldman Sachs expects them to hike by 25 bps in March and to do so until July. Needless to say, the equity market didn’t like this one bit. With earnings already under pressure, a recession is the last thing that the market would want to face. In that respect, according to a recent survey, market pundits have somehow shifted their expectations for a recession to the second half of the year. In the first report relative to 2023, Oracle’s revenues came in line, although their report overall was disappointing; so far there is probably enough growth for companies to meet their estimates. Eventually, yields did come down in the end, with the 2Y yield shedding 50 bps in the week – this only happened in 2001 and 2008 and is seen as a predictive indicator of a coming recession. We probably won’t get a clear direction until we have gotten past the top in rates, and a hawkish Fed definitely isn’t helping – which means that (sadly) we’ll be on the rollercoaster for a while still. Hang in there!

Checking up on the economy: the good

The ‘good’ points to more sustained growth and no recession, albeit at the cost of higher rates (the ‘higher for longer’ moniker that is soon becoming a mantra). Once again, there was not much to report on the good side, so I had a look at Goldman Sachs’ scenario for the year. My issue is that was made with the previous set of expectations on rates, which have since moved twice, so I just wonder if soon we will get an updated scenario with downward revisions to EPS and S&P 500 target price …

Source: Goldman Sachs

Goldman Sachs’ optimism is echoed by the Atlanta Fed GDPNow real GDP Estimate for 1Q23, which sees a growth of 2.0%, revised downward from 2.3% last week. I further note that the average of Blue Chip Consensus, while far away from that projection, has turned positive and so we are getting away from a recession.

Source: Blue Chip Economic Indicators and Blue Chip Financial Forecasts

Share repurchases have been strong so far and remain one of the companies’ favorite use of cash. So far 2023 is well ahead of the past two years as well as of the three-year average.

Source: J.P. Morgan

Finally, I would add that there is evidence that the bellwethers are propping up the S&P 500’s valuation, while that of the whole market remains attractive. The chart below shows that, while we are far away from the excesses demonstrated during the financial crisis, the valuation of the bottom 450 stocks in the S&P 500 can be deemed attractive, That is probably why corporate America is so keen to buy back its own stock.

Source: FactSet, BofA US Equity & Quant Strategy

Checking up on the economy: the bad

There are lots of pressures on rates everywhere you look (that is, US and EU, and excludes Japan, at least for the time being). We’ve had another NFP which came ahead of consensus, in synch with the ADP jobs report a couple of days earlier, and never mind that the jobless claims were also ahead of consensus for the first time. No matter how you look at them, rates are headed higher; and it is very interesting to note the bond yields coming down across the markets on Friday. We start delving into the data with a look at the Fed Funds’ projected direction.

Source: BofA Global Investment Strategy, Bloomberg

There has been a gain of 75 bps in the space of a month, or of a couple of NFPs. Let’s have a look at the spread between 2 Years and 10 Years – clearly indicating a recession – and at the US Government Bond Curve, where the short end moved in synch with the new expectations of further hikes by the Fed.

Source: The Daily Shot

In the chart below you can see how the market’s pricing changed in the last month. The peak rate, which we were debating probably might not even reach 5%, now is in sight of 6%. So many changes over such a short period of time.

Source: The Daily Shot

Speaking of which, the probability that the Fed might hike by 50 bps completely changed after Governor Powell’s testimony, which did not rule out the possibility should the data warrant it. Let’s see the CPI, but I still think it might be better for the Fed to continue hiking rates by 25 bps perhaps for longer, coinciding with Goldman Sachs’ forecast of 5.50-5.75% in July. Still, that is a target based on what we can presently see; an excursion to 6% cannot be ruled out at the moment. If it takes 6 months or more for the market to digest the hike in rates, I think we can forget about having positive results in Equities in the first part of the year and have to rely on the second half (and no recession) in order to salvage the year.

Source: The Daily Shot

Checking up on the economy: the ugly

Equities diverging from bonds is not going to bring the market any favors. Of the two, I think that bonds will be the ones to recover first once we get to a confident terminal rate – though it will take two-three months of successive data to reach that point. Equities will need a lot of confidence – and earnings – in order to get out of the hole in which they are at present.

Source: The Daily Shot

But that’s not the only indicator that raises eyebrows, unfortunately, The inverted 10 Year- 2 Year curve is also pointing to a recession, and has an excellent track record in predicting those. It is showing that a recession will start 6 months from now. This time is different? I hope so, but it pays to be careful.

Source: Bloomberg Finance L.P., Deutsche Bank

Morgan Stanley’s Market Sentiment Indicator has been negative for a while, and so far has proved to be very accurate in 2023. It continues to be negative at present.

Source: Bloomberg, Datastream, Morgan Stanley Research

Finally, we are probably in a phase of the market where the latter is very sensitive to any changes in interest rates, There is an interesting comparison with the past, with the years between 1966 and 1978 when Equity performance was closely tied to whether the Fed was hiking or cutting rates. This chart takes into consideration the Dow Jones Index, which of the three US Indices is the one which had the worst performance YTD. This does underscore my view that meaningful progress is unlikely until the picture of rates becomes clearer.

Source: BofA Global Investment Strategy, Bloomberg

Sentiment and what the market is telling us

Fear and Terror go hand in hand with blood, and unfortunately, there has been a lot of that last week. Following a horrible week, the Fear and Greed Index has moved to Extreme Fear, with a reading of 24, down from last week’s reading of 55. This will chill some spirits for a while.

Source: CNN Business

According to the AAII Sentiment Survey, bears were in the relative majority last week. The survey reflects the uncertainties present in the market, which are particularly ominous for Equities.

Source: AAII Sentiment Survey

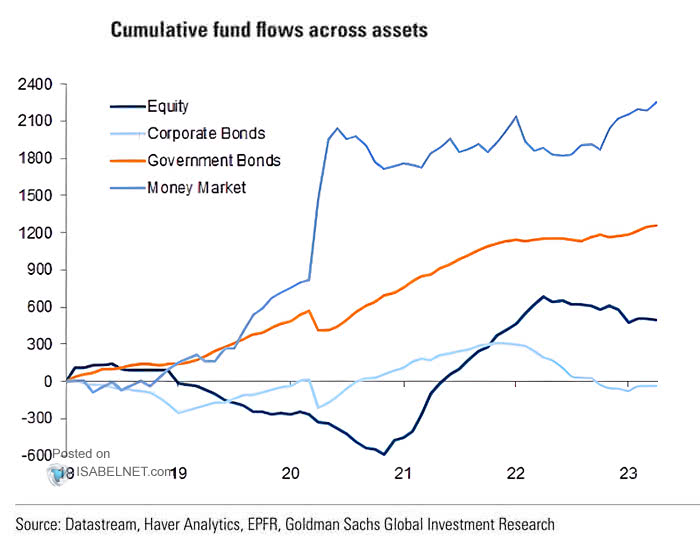

What are the Flows telling us?

Flows to corporate and government bonds have been very strong in the face of uncertainty. Equity seems to do less well after a good start, And with the yields currently offered by money market funds, there is no question that these will get a bid, too. In this environment, cash is king.

Source: Datastream, Haver Analytics, EPFR, Goldman Sachs Investment Research

Another chart reports strong flows toward Treasuries, attracted by the great yields currently paid by the US Government.

Source: BofA Global Investment Strategy, EPFR

Earnings Review

Source: FactSet

The forward 12-month P/E ratio for the S&P 500 is 17.2x, down from last week’s reading of 17.5x, which is below the 5-year average at 18.5x and below the 10-year average at 17.3x. Reporting for 2022 is now complete, and we are looking forward to 2023. The present, bottom-up level is more or less level with Goldman Sachs’ top-down $224 forecast. As we have been going down steadily for a while, I just wonder if at some point down the year the US Corporates will find in them what it takes to reverse this trend, as forecasted to happen in the back half of the year.

For 1Q23 the forecasted EPS decline for the S&P500 on aggregate is -6.1%. If correct, it will mark the biggest decline since 2Q20, when such a decline was -31.8%. The revision to 1Q23 earnings growth has been brutal as it was only -0.4% on Dec 31. Despite the concern about a possible recession next year, analysts still forecast a positive growth in earnings for the overall market in CY 2023 of 1.9% year on year, again revised downwards from 2.1% last week, versus 4.5% on Dec 31, while revenue is forecasted to grow by 2.1% vs 3.3% on Dec 31. The cuts on the S&P 500’s earnings growth are getting significant: earnings growth has more than halved in just 10 weeks since December 31st. Ouch!

Source: Factset

Very few sectors are holding up estimates relative to 31 December. The only sector not to have its estimates cut further is Utilities and – perhaps surprisingly – Communication Services; all the others are facing cuts. After a few disappointing earnings reports Technology has seen its earnings estimates reduced to a mere 0.9% from 3.5% a little more than two months ago.

Source: Factset

The S&P 500 has its revenue growth estimates slightly increased to 2.1% from 2.0% one week ago. Financials are still leading the pack in terms of revenue forecasts, but the only sectors with higher revenue growth than on 31 Dec 22 are Real Estate and Consumer Staples, with all others being down. Information Technology revenue growth has been cut to 1.9% from 3.7% two months ago. The sector seems to be doing better on the top than on the bottom line, perhaps signaling the reason for some of the layoffs; Meta has continued with another round of ‘thousands’ after the reductions in November.

Source: Factset

Let’s take a look at EPS for 2023 and 2024, which last week has the first upward revision in quite a while. The forecast for 2023 has now been updated to $222.92 from last week’s reading of $222.91; while 2024 is currently forecasted to be $249.06, compared to last week’s reading of 248.91. I look with much interest at further revisions as the 1Q23 report season gets underway in March.

Source: Factset

This is the detail for 1Q23. While the market might be more concerned about rates and recession than earnings at this point, the latter’s deterioration is continuing to get me worried as the downward revisions have been relentless and guidance very muted. It seems almost a miracle that the market managed to stay afloat with these shrinking earnings. 4Q22 is over, but 1Q23 looks to start much in the same fashion, with a significant earnings decline. March will see the beginning of the reporting for 1Q23, and I will be looking at it with much interest.

Earnings, What’s Next?

The earnings season is now wrapping up its 4Q22 reports. Highlights this week include Adobe (Wednesday, After Close), and FedEx (Thursday, After Close), which I’m going to look at very closely to see if there is any sign of a weakening economy given the high correlation between freight and GDP.

Source: Earnings Whispers

Market Considerations

Source: Datastream, Haver Analytics, EPFR, Goldman Sachs Global Investment Research

Revenue growth estimates for 2024 are forecasted to grow by 5.0% (4.7% on Dec 31st) and earnings growth estimates for 2024 are predicted to grow by 11.8% (10.3% on Dec 31st), so the future looks to be bright. While we continue to debate whether the US economy will fall into a recession or not and what will be the peak rates for Fed Funds, we should take note that almost every strategy has seen a more defensive positioning in the last month.

The NFP did swing the pendulum in favour of risk off and we are looking at the CPI and PPI to provide more data to complete the picture. Tactically I suggest being short on risky assets, keeping in mind the S&P 500’s 2nd February peak of 4,179.76 as a level which – if broken – would prompt me to cover the trade. For the less volatility prone of you, it may make sense to take all opportunities to lighten up in equities and reinvest in bonds at attractive (approx 4%) yields. For those willing to look besides US treasuries, investment grade bonds (LQD ETF) could also be a valid compromise: 1.2% pickup over government bonds for the safest part of the credit complex may still be compelling. 10-Year yields were turbulent last week, both in the US and Europe, though the ceiling should be near for both. For those wishing to keep their money in Equities, suggest switching to Japan (the country with the more precise picture of rates at the moment) until rate perspectives become clearer in the US and Europe.

Happy trading and see you next week!

InflectionPoint

Disclaimer

All views expressed on this site are my own and do not represent the opinions of any entity with which I have been, am now, or will be affiliated. I assume no responsibility for any errors or omissions in the content of this site and there is no guarantee for completeness or accuracy. The content is food for thought and it is not meant to be a solicitation to trade or invest. Readers should perform their investment analysis and research and/or seek the advice of a licensed professional with direct knowledge of the reader’s specific risk profile characteristics

Leave a Reply