Stocks up, rates up, and bonds struggle but recover some ground on Friday. Europe queen of the week, NDX past Feb 2nd peak. Stay long on (US) Equities, neutral on Bonds, and watch the upcoming data (NFP, Unemployment) carefully.

Major market events 3rd April – 7th April 2023

Highlights for the week

Mon: CH CPI, German Manufacturing PMI, UK Manufacturing PMI, US ISM Manufacturing PMI.

Tue: US JOLTs Job Openings.

Wed: German Factory Orders, EU Services PMI, UK Services PMI, US ADP Nonfarm Employment Change, US ISM Non-Manufacturing PMI.

Thu: German CPI, US GDP, US Initial Jobless Claims.

Fri: US Non-Farm Payrolls, US Unemployment Rate (Markets Closed).

Performance Review

- A clearly positive week for equities, with the worries about yet another banking crisis (Deutsche Bank) clearly put to rest, at least for now. Europe led the rebound, but once again the Nasdaq’s performance was impressive.

- Growth continues to do well over value; the unstoppable Nasdaq 100’s staggering performance YTD continues to crush every other major index (best quarter since 2020) and has now topped its previous peak on Feb 2 (12,803.14), calling for more highs; this does not point to a recession.

- Interestingly, market pundits seem to believe that we are very close to a top in rates; in a recent survey most participants said that the Fed has only 25bps of hikes ahead (I was among the hawks at 50bps); the market is discounting 2 rate cuts before the end of the year clashing with Governor Powell’s statement that he does not see this happening.

- The Fed has expanded its balance sheet by $370 Bn in March alone to over $8.9 Tn, its highest since last November. There is usually a positive correlation between an expansion of the Fed’s balance sheet and the S&P 500’s performance.

- Goldman Sachs has increased the probability of the US having a recession from 25% to 35% after the SVB crisis but notes that they are well below consensus at 60%+.

- A relatively quiet period for earnings, but it seems that 1Q23 won’t be the disaster that many feared. Steady as she goes (the US Economy). I chatted recently with the CEO of an Air Freight business, and he told me that 2Q23 will be ok; he just doesn’t know where demand will be in the back half of the year. This, in his opinion, points to a recession (which is the consensus view), but it could be a case of a mere lack of visibility. We shall see as we go.

Checking up on the economy: the good

The ‘good’ points to more sustained growth and no recession, albeit at the cost of higher rates (the ‘higher for longer’ moniker that is soon becoming a mantra). Rates are probably the most important aspect in that respect, as they continue to create both a ceiling and a headwind for the stock market. The tricky part to navigate is that the market has its views and the Fed has its own, which might be different from the market. Governor Powell has said time and again that the Fed is not worried to hike rates above what is priced by the market and keep them higher for longer if that happens to tame inflation. The market disagrees, however, and you can see it clearly in this chart, showing the market’s pricing of 2 rate cuts before the end of the year, trying to anticipate the Fed. Who will be the first to budge?

Source: Bloomberg, as of 31 March 2023

As a comparison, this is the same chart taken just before the regional banking crisis (SVB). The market believes this will force the Fed’s hand in lowering rates sooner than it had in mind.

Source: Bloomberg, as of 9 March 2023, before the collapse of SVB

This is positive for US Equities as often the market rallies after the last Fed Hike. There is also to consider the positive relationship between the expansion of the Fed’s balance sheet and the performance of the S&P 500, and that it expanded further by $370Bn in March.

Source: BofA Global Investment Strategy, Bloomberg

Source: Real Investment Advice

Next, we have an update from Atlanta Fed on its GDPNow real GDP Estimate for 1Q23, lately at 2.5%, which would be a very positive result. It is worth noticing that the Blue Chip Consensus also reported here, has trickled up to a level of almost 1%. There is still some distance between the two but the direction seems the same.

Source: Blue Chip Economic Indicators and Blue Chip Financial Forecasts

Last but not least, Big Tech is back in vogue. While some say that the market’s leadership might have well been limited so far, the market does need a leader for it to go higher. The rest of the market has plenty of time to catch up.

Source: BofA Global Investment Strategy, Bloomberg

Checking up on the economy: the bad

Let’s start with this chart with a very useful reminder: earnings do not survive recessions. So we absolutely must avoid one if we are to thrive. The pressure on earnings is one of the most concerning aspects to consider, along with an Equity Research Premium well away from its usual standard.

Source: Real Investment Advice

And the likelihood of getting one – calculated from the yield curve – is greater than 60%. This is also the consensus among economists, though Goldman Sachs thinks the real probability is only 35%.

Source: Federal Reserve Board, Federal Reserve Bank of Cleveland, Haver Analytics

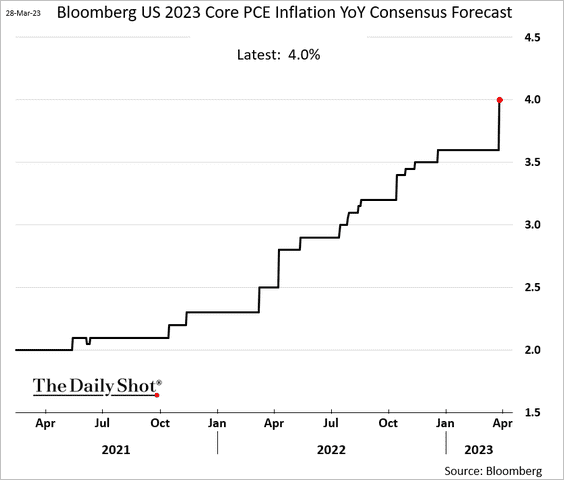

Another thing to worry about is the Fed’s arch-nemesis: inflation. It certainly does not help that it is taking a long time to decline, and might be even revised upwards, as it happened to this 2023 Core PCE Consensus Forecast, recently updated to 4%.

Source: The Daily Shot, Bloomberg

Checking up on the economy: the ugly

One of the major issues with the market is valuation and the pressure earnings face (remember the recession?). Until we get 1Q23 results for some relevant companies (and it might take us the entire month of April to get us there) we won’t have a feeling of much pressure they have to withstand. And – as usual, in terms of earnings – opinions differ wildly. Morgan Stanley (which has one of the most bearish forecasts on the street for S&P 500’s at $195 for 2023) reminds us that there is a disconnect between the Equity Risk Premium and the earnings growth. Something’s got to give.

Source: FactSet, Bloomberg, Morgan Stanley Research

Another worry is that the leadership shown so far by the S&P 500 has been limited to a very small group of stocks – 5. Eventually, the rest of the market will have to catch up if we are to have a more stable and robust leadership.

Source: Goldman Sachs

Finally, ROW stocks are doing much better than the US when it comes to the dividend yield. So far there has been enough growth to sustain the market, but this could become relevant were the recession to materialize.

Source: Topdown Charts, Datastream

Sentiment and what the market is telling us

The Fear and Greed Index has improved from Fear to Neutral, ending the week with a reading of 49, revised upwards from last week’s reading of 33. It seems to lift in synch with the market’s moves.

Source: CNN Business

A slightly different picture is offered by the AAII Sentiment Survey. Bulls have increased, and Bears have decreased, but not by that much. The Bears still are in control; let’s see if this will be true even after Friday’s Non-Farm Payroll.

Source: AAII Sentiment Survey

Here is a list of the best-performing stocks of 1Q23 in the US. Nearly all of them belong to Information Technology.

Source: Investing.com

What are the Flows telling us?

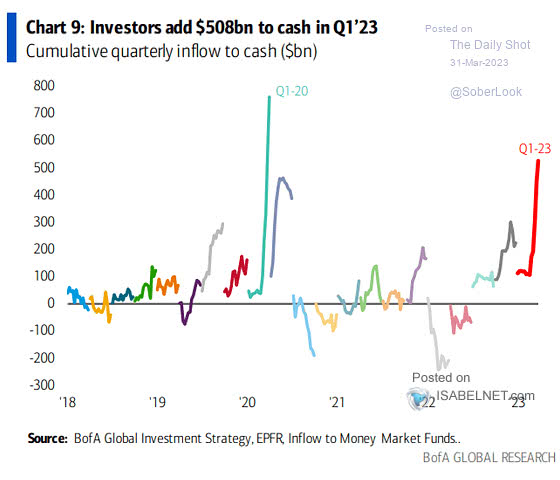

Cash is being upgraded from king to emperor, or even tsar. Some say this is the next speculative bubble (!), which is why interest rates will fall. I thought the central banks’ main mandate was to fight inflation, not to reduce yields of savers who, quite frankly, had it tough for so many years (remember negative yields?). As long as these rates are going to last, inflows are going to continue.

Source: BofA Global Investment Strategy, EPFR

Notwithstanding the strong performance YTD, there have been outflows in Equity funds. While households will be sellers of Equities in 2023, this will be compensated by investors, corporate buyers, and buybacks.

Source: EPFR Global

Earnings Review

Source: FactSet

The forward 12-month P/E ratio for the S&P 500 is 17.8x, up from last week’s reading of 17.1x, which is below the 5-year average at 18.5x but above the 10-year average at 17.3x. Reporting for 2022 is now complete, and we are looking forward to 2023. The present, bottom-up level ($221.5) is beginning to slip from Goldman Sachs’ top-down $224 forecast. As we have been going down steadily for a while, I just wonder if at some point down the year the US Corporates will find in them what it takes to reverse this trend, as forecasted to happen in the back half of the year.

For 1Q23 the forecasted EPS decline for the S&P500 on aggregate is -6.6%. If correct, it will mark the biggest decline since 2Q20, when such a decline was -31.8%. The revision to 1Q23 earnings growth has been brutal as it was only -0.3% on Dec 31. Despite the concern about a possible recession next year, analysts still forecast a positive growth in earnings for the overall market in CY 2023 of 1.5% year on year, revised downwards from 1.9% last week, versus 4.5% on Dec 31, while revenue is forecasted to grow by 2.0% vs 3.2% on Dec 31. The cuts on the S&P 500’s earnings growth are getting significant: earnings growth has been reduced to a third of what it was just 12 weeks ago. Ouch!

Source: Factset

Very few sectors are holding up estimates relative to 31 December. The only sector not to have its estimates cut further is Utilities and – perhaps surprisingly – Communication Services; all the others are facing cuts. After a few disappointing earnings reports Technology has seen its earnings estimates reduced to -0.5% from 2.6% a little more than three months ago.

Source: Factset

The S&P 500 has its revenue growth estimates stable from last week at 2.1%. Financials are still leading the pack in terms of revenue forecasts, but the only sectors with higher revenue growth than on 31 Dec 22 are Real Estate and Consumer Staples, with all others being down. Information Technology revenue growth has been cut to 1.9% from 3.7% two months ago. The sector seems to be doing better on the top than on the bottom line, perhaps signaling the reason for some of the layoffs; Meta has continued with another round of ‘thousands’ after the reductions in November.

Source: Factset

Let’s take a look at EPS for 2023 and 2024, which last week has the first upward revision in quite a while. The forecast for 2023 has now been updated to $221.50 from last week’s reading of $222.75; while 2024 is currently forecasted to be $248.16, compared to last week’s reading of 248.74. I look with much interest at further revisions as the 1Q23 report season gets underway in April.

Source: Factset

This is the detail for 1Q23. While the market might be more concerned about rates and recession than earnings at this point, the latter’s deterioration is continuing to get me worried as the downward revisions have been relentless and guidance very muted. It seems almost a miracle that the market managed to stay afloat with these shrinking earnings. 4Q22 is over, but 1Q23 looks to start much in the same fashion, with a significant earnings decline. April will see the beginning of the reporting for 1Q23, and I will be looking at it with much interest.

Earnings, What’s Next?

The earnings season is now entering its early 1Q23 reports. Here’s a list of companies reporting this week.

Source: Earnings Whispers

Market Considerations

Source: Topdown Charts, Thomson Reuters Datastream

Revenue growth estimates for 2024 are forecasted to grow by 5.0% (4.6% on Dec 31st) and earnings growth estimates for 2024 are predicted to grow by 12.1% (10.2% on Dec 31st), so the future looks to be bright. While we continue to debate whether the US economy will fall into a recession or not and what will be the peak rates for Fed Funds, we should take note that almost every strategy has seen a more defensive positioning in the last month.

We are probably shifting from a monetary risk to a macro risk, as shown by the chart above. We should be mindful that the economy is probably just doing ok, even though passing the peak in rates will remove the overhang present on the market. If and when rates will diminish in importance, earnings (and top-line growth) will pick up their pace.

The Nasdaq has been able to climb above its peak of 12,803.14 on 2nd February, and now it’s time for the S&P 500 to follow through (its peak is 4,179.76 on the same day). Tactically continue to suggest staying long on US Equities, keeping in mind the S&P 500’s 5th January bottom of 3,808.10 as a level which – if broken – would prompt me to cover the trade. European Equities seem to be ok, too – avoid the UK as it is a chronic underperformer. Regarding bonds, the trajectory is that yields will eventually fall, albeit with a few bumps on the road. As we are still gathering data in that respect I prefer to stay on the sidelines for the time being.

For the less volatility prone of you, it may make sense to take all opportunities to alter the weights of your asset allocation by increasing the weights of safety assets at the expense of more risky assets by lightening up in equities and reinvesting in bonds at attractive (approx 4%) yields. For those willing to look besides US treasuries, investment grade bonds (LQD ETF) could also be a valid compromise: 1.2% pickup over government bonds for the safest part of the credit complex may still be compelling. 10-Year yields were turbulent last week, both in the US and Europe, though the ceiling should be near for both. For those wishing to keep their money in Equities with lower volatility, suggest switching to Japan as the company with the most stable outlook (the country with the more precise picture of rates at the moment) until rate perspectives become clearer in the US and Europe.

Happy trading and see you next week!

InflectionPoint

Disclaimer

All views expressed on this site are my own and do not represent the opinions of any entity with which I have been, am now, or will be affiliated. I assume no responsibility for any errors or omissions in the content of this site and there is no guarantee for completeness or accuracy. The content is food for thought and it is not meant to be a solicitation to trade or invest. Readers should perform their investment analysis and research and/or seek the advice of a licensed professional with direct knowledge of the reader’s specific risk profile characteristics.

Leave a Reply