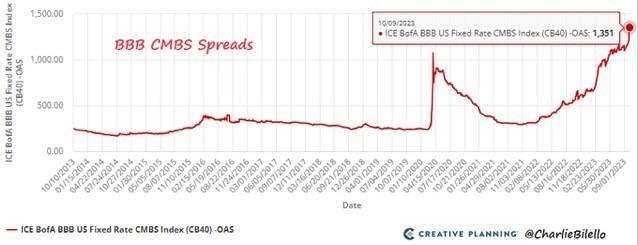

The spreads on BBB-rated CMBS (commercial-mortgage-backed securities) have surged to 1,351 basis points, marking their most significant increase in over ten years. This rise reflects bond investors’ anticipation of an impending wave of defaults

As this unfolds, American banks, significant holders of US government bonds, are poised to witness mounting unrealized losses in their portfolios as a result of the sudden surge in US Treasury yields.

@inflectionpoint: We completely concur with P. Tudor Jones. We’re in the midst of the most perilous geopolitical situation since World War II, all the while grappling with the most fragile fiscal condition in decades. We believe financial instability coupled with a sovereign debt crisis, in those countries with the weakest debt and fiscal positions, might be quietly resurfacing! Check out the charts by Bilello & S&P Global.

Leave a Reply