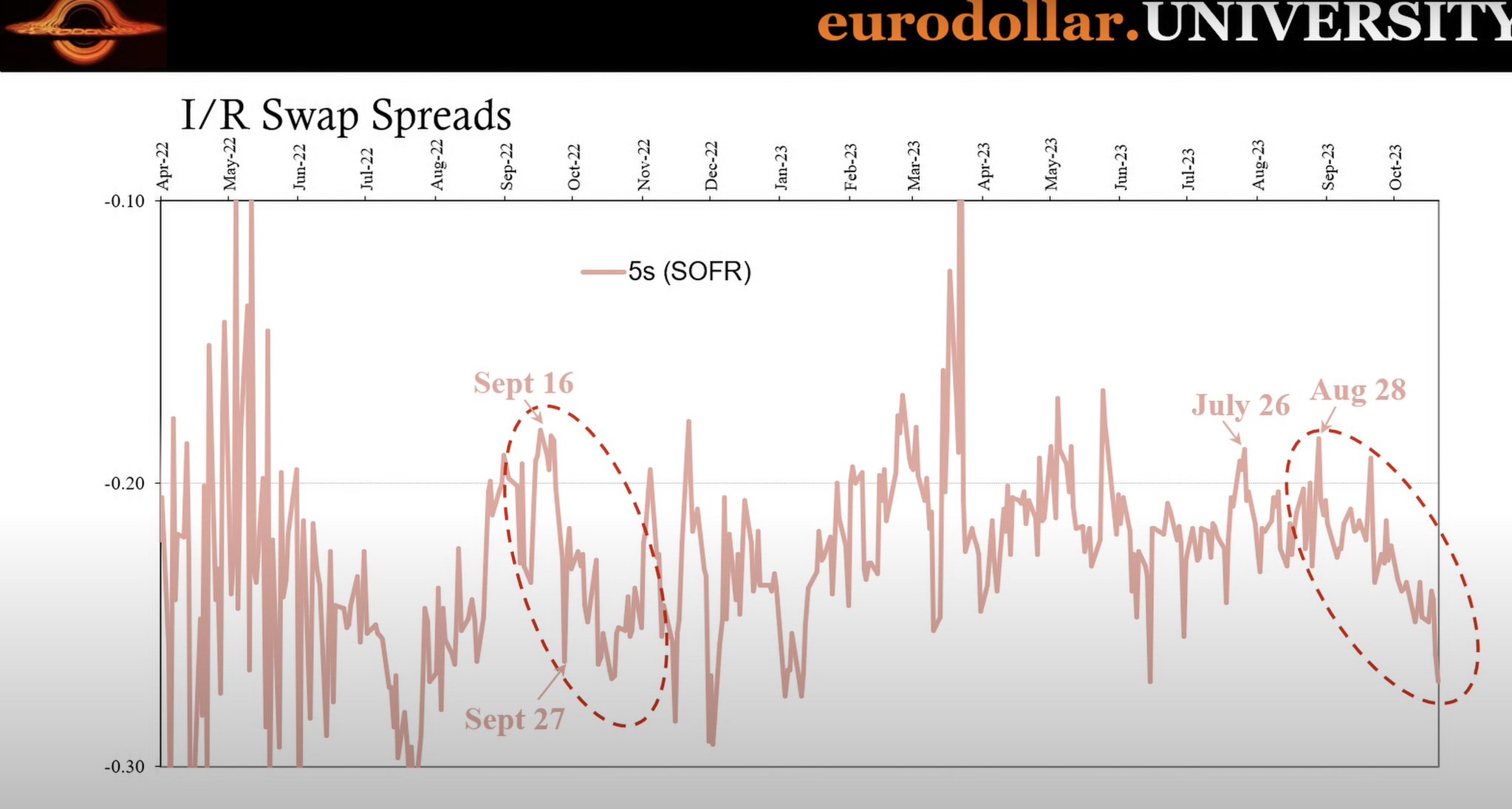

Turmoil in Swap Spreads is often a canary in the coal mine!

Negative swap spreads occur when the fixed payment on swaps is lower than the yield you get from US Treasuries of the same maturity. Swaps paly a crucial role for banks and pension funds in managing the rates risk of their large books!

But what does it really mean?

A 2018 study conducted by the Federal Reserve Bank of New York solidified the connection between negative swap spreads and the constraints faced by dealers. The findings suggested that when swap spreads take a downward turn, it clearly indicates the challenges dealers encounter in meeting capital requirements and effectively managing perceived escalating risks.

Moreover, a separate study in the same year, undertaken by the Bank for International Settlements (BIS), highlighted the significant involvement of underfunded pension plans in the demand for interest rate swaps. These plans strategically employ swaps to safeguard against duration risk, particularly during financial instability. Consequently, the implications of negative swap spreads transcend mere dealer predicaments, encompassing a more extensive panorama of financial upheaval within the ecosystem.

Given this complex financial landscape, at #InflectionPoint we believe that this development signifies a capitulation by the bond market’s bullish players, who have been building up long positions since the beginning of the year! Given the prevailing precarious geopolitical climate, we think this represents an inflection point and further reinforces the necessity of adopting a tactically long-duration strategy, marking the awaited signal for such a move.

Chart by Jeff Snider

InflectionPoint @GiorgioVintani & @TomBaldacci

Leave a Reply