After the monumental last week, in which yields decreased sensibly from their peak, it is useful to provide an update about the market. Recall that I advised the bravest of you to re-enter equities with a 3% weekly stop. There are a few relevant data points this week, apart from the speeches by Fed Chair Powell today and tomorrow and the inflation data from China tomorrow, in preparation for US CPI and PPI next week which could be a game changer.

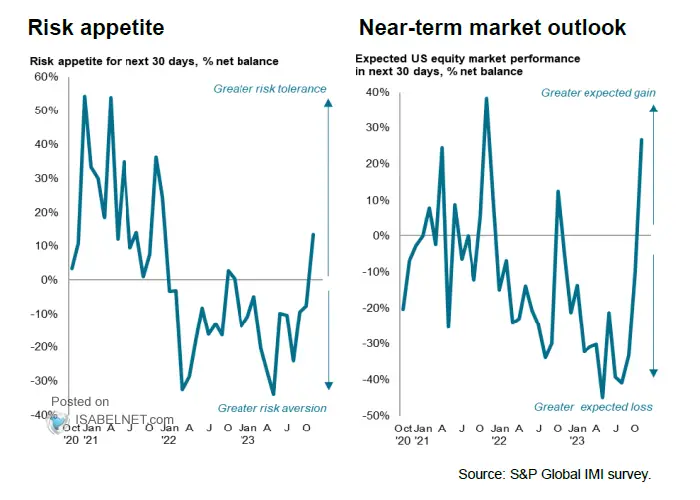

Contrary to CNN Business’ Fear and Greed Index, which is still in Fear (41), S&P reported a more constructive attitude to risk appetite and near-term outlook. Granted, the seasonality effect might well play a role here, although some market pundits are questioning whether we will see a year-end rally at all. I think that rates are probably key here – and the recent moves in the US 10-year bond have been encouraging to that end. The present valuations, while high, could be sustainable if the bond yields moderate further.

Introducing the latest forecasts on the long bond yield by Goldman Sachs. Goldman’s highly respected economics team sees a decline in yield for the long bond greater than the market’s current assessment. This is due to the expected disinflation that should take place in the US in 2H23 – and we’ll get a feeling for that next week with the key CPI and PPI data. It is clear that such a scenario, coupled with the modest (+5%) EPS growth they are forecasting, would be positive for equities. Something we shouldn’t forget is that 2024 will be an election year in the US – and so far the news has been relatively quiet, even though the debate will certainly heat up once the primaries are in place.

Having a look at the median sector returns in the year leading to the elections, I note a good performance by utilities, while technology underperformed. It is too early to see how the political debate unfolds, but I would think that things could be different this time, as interest rates are supposed to go down, not up. By November next year, we might witness a few cuts by the Federal Reserve, helping to sustain the market. And of course, much will depend on whether the victory will go to a Democrat or to a Republican (and by how much), as the two parties have vastly different agendas and policies.

Finally, the relative consistency of the short interest – which had a mild increase since 2021, helps in assessing the present situation and in ruling out yet another bubble, apart from a few hyped companies (my assessment of the Magnificent 7 is not equal for all of them), namely Tesla and Nvidia. At their current valuation, they are priced for perfection, so handle them with care.

Provided that the inflation data does not tell us otherwise, these are some of the supporting reasons for a more constructive positioning into year-end. Traditionally, the fourth quarter is the strongest for many of the S&P 500 companies, which means that while execution will be very important, all the fundamentals seem to be in place. As usual, prudent risk management is key, so set it at 3% on a weekly basis and respect it, as timing is notoriously difficult to second guess.

Charts from S&P Global and Goldman Sachs H/T ISABELNET.com

Leave a Reply