We’ll remember yesterday, and this week, for a long time as the key week in determining the outlook for the markets in the near term. 3 major central banks – the ECB, the BOE, and last but not least the Fed – all paused their hiking cycles. (The BOJ didn’t, but Japan is the country with the lowest rates and their relaxing of YCC controls is unlikely to throw a spanner in the works). But there is more: the Fed might have finally ‘pivoted’ by suggesting they are discussing whether to increase rates even more, as opposed to a sure thing. So it is quite possible that the peaks in rates are now behind us (with the possible exception of Japan), and that rates are due to fall from here (Japanese rates are also falling today).

The S&P 500 is now having a comeback, after conquering the Feb 2 peak of 4,179.76, bolstered by lower rates. The Atlanta Fed GDPNow updated for 4Q23 is now only seeing a growth of 1.2%, a significant contraction from 2.3% recorded on Oct 27. This has led some experienced market pundits (thanks Carlo!) to speculate that 3Q23 was the last quarter with super growth and that it would moderate, perhaps substantially, from here, causing rates to fall.

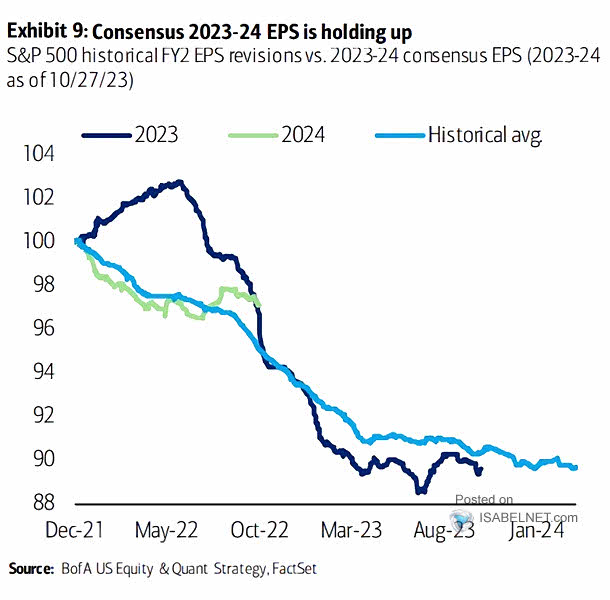

There are, however, a couple of important checks on this world-leading index. According to the chart below, consensus EPS for 2023 and 2024 is holding up. This will allow the index to reduce its valuation and possibly find some upside especially if rates are headed further down – goodbye to TARA (There Are Real Alternatives), welcome back to TINA (There Is No Alternative)?

And yet there is more to underscore that here we really have a gorilla in the room. The chart below highlights the S&P 500’s magnificent performance as an asset class, despite the tough last 3 months.

And yet there is more to underscore that here we really have a gorilla in the room. The chart below highlights the S&P 500’s magnificent performance as an asset class, despite the tough last 3 months.

Despite the correction, the American index has cemented its position as the asset class with the best return to date. Charles Dow’s famous quote: ‘The trend is your friend’ might well apply here. Especially if, notwithstanding everything, earnings continue to do well.

Speaking of which, Apple is going to report tonight after close. Fingers crossed …

Charts from Bank of America. H/T ISABELNET.com

Leave a Reply