Yields on the long bonds are falling and off their highs, particularly after a benign CPI and PPI. This has prompted a rally of both bonds and equities and completely wiped out any chances that the Fed might hike again in December and in January (the CME FedWatch tool has an almost perfect consensus – 99.8% – for staying the course and pausing), with the first cut being anticipated to May. I have long been of the opinion that the long bond tends to anticipate any move by the Central Bank, and so, in order to find out what happens in Washington, just look at it.

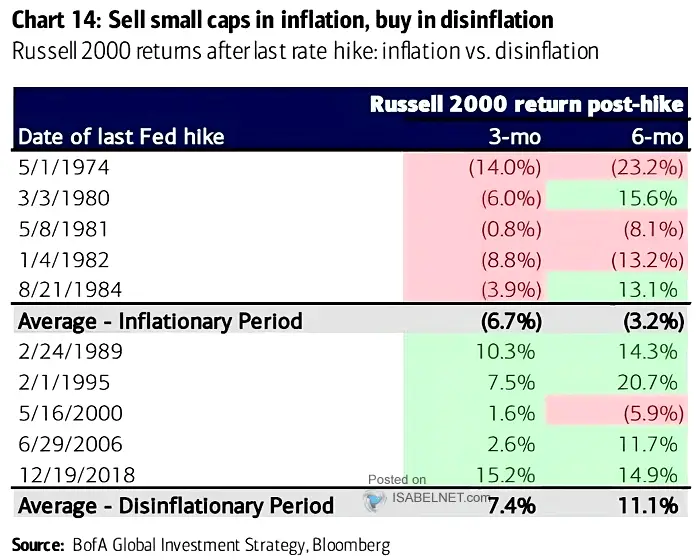

On the day in which there was a massive rally, none shone more than the Russell 2000, the benchmark for small caps. The chart below states that small caps do best in disinflation, and hence might be one of the ways to approach an investment in equities in 2024. Most economists are pivoting towards ‘no landing’ (continued strength in the US economy) and to growth, albeit more subdued, in corporate earnings. In other words – more of the same, but with significantly lower rates (on the 10-year treasuries long before than on Fed Funds). Take a look at them – not just in the US, but in Europe as well – as yields start to fade.

Charts from Bank of America. H/T ISABELNET.com

Leave a Reply